The sale of Movistar Mexico to the Melisa Acquisition consortium (US$450 million for an operator with approximately 15% of the market) closes a chapter of more than two decades in which the Spanish operator invested over €3.6 billion only to end up competing, at a permanent structural disadvantage, against a monopoly that has never ceased to be one.

Why it matters. One might think that Telefónica’s departure changes the Mexican telecommunications market, but the reality is that it doesn’t change it much. On the contrary: it confirms it.

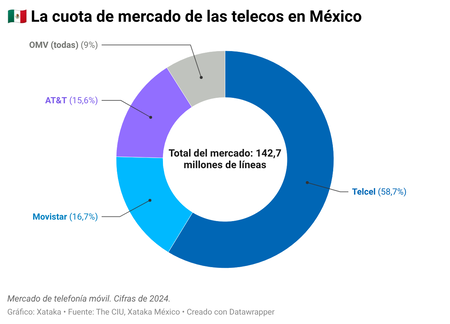

Mexico has one of the most concentrated mobile markets in the developed world, with Telcel, owned by Carlos Slim, controlling almost 60% of users. No competitor has managed to steadily gain market share this century. What’s strange is that Telefónica took so long to leave the country, because it only did so in the context of a complete withdrawal from Latin America after years of losses.

The backdrop. Telcel inherited the commercial muscle, infrastructure, and customer base of Telmex, the former state monopoly privatized in 1990. Since then, Mexican regulators have been unable to balance the market, or perhaps lacked the will to do so.

AT&T has been trying for years with its own network and remains below 16%. In fact, it too is looking for a way out. Telefónica, which in 2019 had to return its spectrum and rely on AT&T’s infrastructure to survive, was already operating in practice as a kind of “premium MVNO”: with its own brand, but without its own network and without room to grow.

Between the lines. The buyer speaks volumes. Melisa Acquisition is not a typical telecommunications operator: it is the combination of Oxio (a technology platform for virtual operators with barely 350,000 customers) and an investment fund.

They are not coming to build network infrastructure or to compete with Telcel for market share. They’re simply arriving to manage what’s already there: an inherited customer base, a lean asset model, and the hope that Oxio’s technology will allow them to squeeze a bit more profit out of an operation Telefónica no longer wanted to maintain.

In numbers. The ARPU (average revenue per user) quantifies the trap Telefónica was operating in in Mexico: 64.7 pesos per month per customer, less than half that of AT&T (141.1) and less than a third of that of Telcel (176).

It’s not just that Movistar had few customers; it’s that each customer was worth little in terms of revenue and profitability. Such a model doesn’t allow for investment in the network, spectrum, or future. The sale isn’t an elegant strategic retreat: it’s the logical conclusion of years of competing in the cheapest segment of an already cheap market.

Yes, but. The sale will generate significant accounting losses for Telefónica, something inevitable given the historical outlay, but it fits perfectly into their strategy. In less than a year and a half, the telecom company chaired by Marc Murtra has practically dismantled all its operations in Latin America: Argentina, Chile, Peru, Uruguay, Ecuador, Colombia… and now Mexico.

Only Brazil remains, the only market in the region where Telefónica has sufficient scale to truly compete and which has become one of its growth engines, if not the main one.

The biggest loser? The Mexican consumer. With Telefónica downsized, the Mexican market is even more vulnerable to Telcel. Effective competition in price, coverage, and service quality now depends almost exclusively on AT&T, which has also failed to demonstrate the capacity to challenge Slim’s dominance and, as we have already mentioned, has been seeking an exit for some time.

Mexico isn’t just losing an operator: it’s losing one of the few that at least had an incentive to try.

Source: xataka

{kind=link}